About This Publication

Welcome to my engineering log documenting the development of QuantCoderFS — a unified quantitative research platform for retail traders.

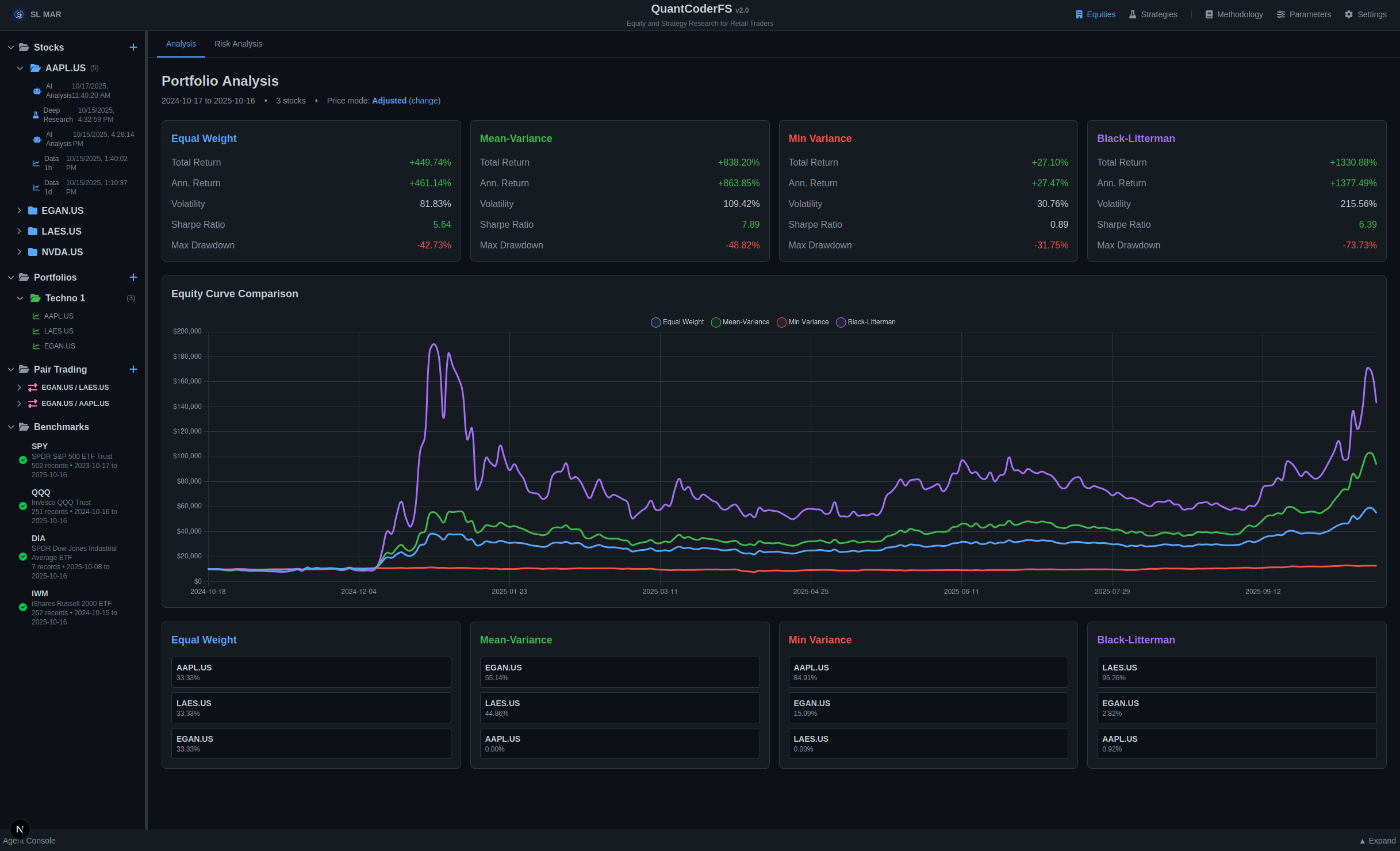

What is QuantCoderFS

QuantCoderFS integrates two core modules:

Market Intelligence Module

Purpose: Multi-agent equity research inspired by MarketSense AI (Fatouros et al., 2024).

Input: Stock tickers (e.g., AAPL.US, TSLA.US)

Output: BUY/HOLD/SELL trading signals with conviction scores (1–10)

Technology: Custom multi-agent system featuring four specialized agents and one orchestrator

Strategy Generator Module

Purpose: Automated trading algorithm creation derived from academic research papers

Input: PDF research papers

Output: Production-ready QuantConnect algorithm code (Python)About This Publication

Welcome to my engineering log documenting the development of QuantCoderFS — a unified quantitative research platform.

Each post shares what truly happens under the hood: successful builds, failed experiments, and everything in between.

Launch planned: February 2026

Documentation: QuantCoderFS Documentation

Who Should Subscribe

This publication is for traders, quants, data engineers, and risk managers who build and run systematic code — or anyone managing real-world positions using algorithmic signals.

As the project evolves, outputs such as equity analyses and strategy research may also be published.